Learn about the most common types of VA entitlement codes found on the Certificate of Eligibility (COE) and how this code impacts your VA home loan eligibility.

The Certificate of Eligibility is not the simplest document to decipher. That's why having a trusted VA lender get it for you is the most common path for VA borrowers.

For veterans and service members who want to know more about their COE, one of the most common questions is about entitlement codes. There are 11 different entitlement codes, and at least one of them will be on every Certificate of Eligibility. These codes help explain the nature of your service and eligibility for the VA loan benefit.

What Are VA Entitlement Codes?

VA Entitlement Codes explain how a veteran or spouse is eligible for the VA home loan benefit by representing a period of military service or alternative entitlement justification. A veteran’s VA entitlement code can be found on the Certificate of Eligibility.

What Does Your VA Entitlement Code Mean?

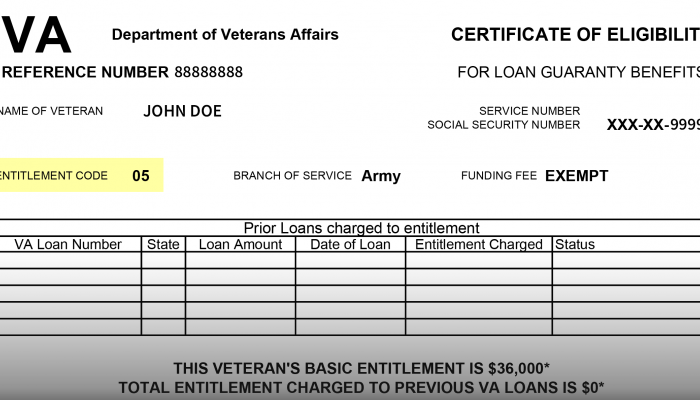

The VA Entitlement code located at the top of the Certificate of Eligibility details the nature of service eligibility for a qualified veteran, active military member, or military spouse.

You may have seen your entitlement code before, wondered what this code means, and how exactly it describes your service. For example, what does it mean when a veteran has an entitlement code of 05?

The following table translates your code into plain English:

Full List of VA Entitlement Codes

| Entitlement Code | Era |

|---|---|

| 01 | World War II |

| 02 | Korean War |

| 03 | Post-Korean War |

| 04 | Vietnam War |

| 05 | Entitlement Restored |

| 06 | Surviving Spouse |

| 07 | Spouse of POW/MIA |

| 08 | Post-World War II |

| 09 | Post-Vietnam |

| 10 | Persian Gulf War |

| 11 | Selected Reserves |

VA Entitlement Calculator

Calculate your estimated available VA entitlement and maximum loan amount with 0% down.

Common Entitlement Codes

Let’s break down a few entitlement codes that we get asked about frequently.

Entitlement Code 05

A VA entitlement code of 05 is typically an indication that you’ve used your VA home loan benefit at least once before. The entitlement code of 05 simply states that your entitlement has been “restored” allowing you to use your VA loan benefit again. For example, you can buy a second home with a VA loan using something called second-tier entitlement. Alternatively, you may be trying to use a VA loan again after selling your previous home.

Entitlement Code 10

The majority of today’s veterans who have served on active duty in the last 20-30 years will receive an entitlement code of 10, which signifies an enlisted date during the Gulf War, which the VA has defined as enlistment between 8/2/1990 – present.

Entitlement Code 11

VA Entitlement Code 11 signifies VA home loan eligibility earned by Reservists who’ve met the minimum requirements as set forth by the VA. This includes at least 6 years in Selected Reserves unless you qualify because of activation under Title 10 orders.

No matter what your entitlement code is, if you think you’re eligible for a VA home loan, it’s probably a good idea to verify your eligibility with a trusted VA loan lender.

It's also important to understand that you don't need your Certificate of Eligibility in hand to start the VA loan process. You will ultimately need it to close on a VA loan, but it's something that lenders often get for borrowers once they've already kick-started the process. Nearly all COE requests are electronic, with the bulk of them fulfilled in seconds using the VA's automated system.

Talk with a Veterans United VA Loan Expert at 855-870-8845 for more details.

Related Posts

-

2024 VA Funding Fee: Complete Explainer with Charts and ExemptionsThe VA funding fee is a governmental fee required for many VA borrowers. However, some Veterans are exempt, and the fee varies by VA loan usage and other factors. Here we explore the ins and outs of the VA funding fee, current charts, who's exempt and a handful of unique scenarios.

2024 VA Funding Fee: Complete Explainer with Charts and ExemptionsThe VA funding fee is a governmental fee required for many VA borrowers. However, some Veterans are exempt, and the fee varies by VA loan usage and other factors. Here we explore the ins and outs of the VA funding fee, current charts, who's exempt and a handful of unique scenarios. -

Can Your Mortgage Be Denied After Preapproval?It is possible for you to get denied for a home loan after being preapproved. Find out why this may happen and what you can do to prevent it.

Can Your Mortgage Be Denied After Preapproval?It is possible for you to get denied for a home loan after being preapproved. Find out why this may happen and what you can do to prevent it.